When a truck collides with a commercial building, understanding the responsibilities and processes for repair can be complex yet crucial. Fleet managers and trucking company owners must recognize that liability often falls on the driver and their insurance. Procurement teams in construction or mining need to be proactive in managing repair services post-accident. This article dissects the topic into three comprehensive chapters, beginning with liability assessments, followed by the insurance claims process, and concluding with the roles of construction and repair services. Together, these sections provide a thorough understanding of who is responsible for fixing damaged commercial buildings in the wake of a trucking accident.

After the Crash: Decoding Liability and the Road to Rebuilding a Commercial Building Hit by a Truck

A truck slams into a commercial building, creating obvious safety concerns and a tangle of liability questions. The journey from incident to repair centers on identifying fault, securing insurance coverage, and coordinating stabilization, assessment, and reconstruction while minimizing business disruption. Typically, fault lies with the driver or the employer through auto liability and, when appropriate, vicarious liability. Premises liability may attach to the building owner if maintenance or structural issues contributed to the damage. Insurance then governs the flow of funds: the at-fault party’s insurer funds repairs to the extent coverage allows, with the building owner’s property insurer covering residual costs and facilitating temporary needs, all subject to subrogation rights. The process requires thorough documentation, independent engineering assessments, prompt claims, and clear communication with tenants to manage expectations. Stabilization work, a detailed damage assessment, and a formal repair plan with permits and codes create the roadmap for reconstruction. Legal counsel can help navigate complex subrogation, coverage gaps, and fault questions, while a coordinated team of engineers, architects, and contractors executes the work. In short, liability points to who pays, but the structure of the insurance program determines how funds are mobilized, allocated, and recovered as repairs proceed.

Crash and Fix: Navigating Liability, Insurance, and the Repair Path After a Truck Hits Your Commercial Building

The moment a heavy vehicle collides with a commercial structure, the world you rely on for your business can feel suddenly unstable. Walls crack, storefronts buckle, and the moral of the story abruptly shifts from steady operations to a careful walk through liability, coverage, and the often opaque choreography of repairs. In the minutes, hours, and days that follow, the question you ask most is not simply who caused the damage, but who will fix it, who pays, and how to keep your business functioning while the dust settles. The answer is not a single party stepping forward with a complete remedy; it is a triage of responsibility, insurance alignment, and practical construction management that, if handled deftly, can restore your building with minimal disruption and clear accountability. This chapter follows that path in a narrative that places you, the owner, at the center of the decision making, because in incidents like this the owner does not just observe the process. The owner steers it, negotiates it, and ultimately accepts the outcome with both financial prudence and professional resolve.

The crash begins as a shock, a loud and visible break in the rhythm of daily business. People instinctively check for safety; first responders are summoned; the scene, when permitted, is secured to prevent further harm. It is essential to treat this as more than a momentary accident. It is the point at which safety, law, and finance converge, and from which the entire repair trajectory will emerge. You are not merely a claimant seeking compensation. You are the project lead in a repair that will restore the building to its original function, update its safety compliance, and preserve the business continuity that your tenants, customers, and staff depend on.

From the outset, documentation becomes your most valuable tool. The most immediate actions are practical and precise. Photograph and video the damage from multiple angles, capture the truck and the point of impact, and note the extent of any collateral damage to signage, fixtures, and the structural envelope. Record environmental conditions such as weather and lighting that might influence the assessment. Collect times, dates, and any statements from witnesses on site. The more granular your file, the clearer the path becomes for insurers to evaluate fault and for you to justify repair estimates. The police will typically file an official incident report that codifies the facts on the record. That report, along with the on site evidence, forms the backbone of fault determination, which in turn influences which insurance party should respond to the claim. In many cases, liability rests with the truck driver or the operator’s liability insurer, particularly when evidence shows negligent driving or violation of traffic laws. Yet there are instances where the cause of the crash arises from factors that might implicate the building or surrounding conditions, and those nuances can shift the coverage dynamic in meaningful ways. The important point is not to jump to conclusions in the first hours. The determination of fault is a legal and factual process that unfolds as investigators, insurers, and your own documentation interact.

In parallel with the investigative process, you should notify your commercial property insurer. Even though the truck driver or their liability insurer may ultimately be responsible for repair costs, your own property insurer will usually want to be aware of the incident. They will guide you through the claim reporting requirements, including timelines and documentation. Most policies require you to report the loss promptly or within a defined window, often within 24 to 48 hours. Your insurer will assign an adjuster who evaluates the damage, reviews the repair plan, and calibrates the settlement against policy terms, including deductibles and coverage limits. The interplay between your own policy and the other party’s policy is the core mechanism that channels the financial resources necessary to restore the building. The owner who understands this interplay can better orchestrate the repair process, avoiding delays and misunderstandings that can bleed money and time from the project.

The repair liability itself rests on a simple, sometimes awkward, principle: if the truck driver or their insurer is determined to be at fault, that insurer will typically bear the cost of repairing the building. The argument that a third party caused the damage is straightforward in many cases, but the actual payment pathway involves a negotiation among adjusters, the owner, and the chosen contractors. The owner is not passive in this stage. You will assess estimates, select a contractor, and supervise the repair plan. The insurer approves or adjusts the plan, ensuring that the scope of work aligns with the policy terms and that the proposed costs are reasonable. If you decide to pursue more expensive options or higher quality materials than what the insurer deems standard, you may be responsible for the difference up to the policy limits. This reality reinforces a pragmatic truth: while liability may be attributed to the truck driver or their insurer, the repair outcome is ultimately managed by the building owner with the insurer acting as the financial intermediary. The owner, therefore, must balance quality, cost, and timeline, ensuring that the project remains on track and compliant with code and safety standards while not becoming a discretionary luxury obtained at the expense of fairness to the insurer and to the business.

The question of who fixes the building cannot be settled by blame alone. It is settled by a sequence that begins with the claim and ends with a repaired envelope that returns the business to operating capacity. First, an insurer adjuster arranges a survey of the damage. This is not a mere cursory inspection; it is a professional assessment designed to quantify the loss and determine whether the damage is limited to cosmetic surface issues or extends to critical structural elements, HVAC systems, electrical infrastructure, and life safety components. In many cases, the driver or owner of the truck will be liable for the direct repair costs. In others, your own property policy might respond to cover certain elements if liability shifts or if there are gaps in the coverage of the at fault party. The adjuster will compare the repair estimate against policy coverage and may require you to obtain multiple estimates, ensuring that the scope of work is comprehensive and cost efficient. The intent is to establish a fair and reasonable cost, rather than to reward or punish any party. The insurance process, in this sense, is a framework designed to prevent spiraling costs while protecting the owner from under repair and ensuring code compliant construction.

Crucially, the owner retains considerable agency in the repair stage. The police report and insurer assessments determine who pays, but the owner selects the contractor who will actually perform the work. You may invite contractors of your choice to assess the damage and provide a repair estimate. The insurer will review the estimates, sometimes propose adjustments, and ultimately approve a plan that matches the policy guidance and the needs of the building. The insurer does not supervise the construction on the ground in the manner a general contractor would; rather, they authorize the payment path and ensure that the work performed aligns with the approved scope and budget. As the owner, you coordinate with licensed professionals to deliver the repair work. You have the final say on which contractor executes the project, subject to the funds the insurer has approved. If the approved budget is lower than your preferred approach, you must decide whether to proceed with the insurer’s budget or negotiate a revised agreement with the insurer that either redefines the scope or extends the budget. In most instances, the practical approach is to align your project with the insurer’s assessment of reasonable cost and standard of repairs, while still ensuring that the final result meets code requirements and tenant expectations.

A practical reality emerges early in the process: the repair path is a collaboration, not a confrontation. The insurer provides the money and the oversight to ensure fair costs, but the day to day execution is your responsibility. You hire a licensed contractor, develop a repair schedule, and work with your property management team to maintain business operations during the work. The insurer may arrange direct payment to the contractor or reimburse you after you submit invoices. This arrangement, commonly described as a direct payment or first party payment mechanism, streamlines the flow of funds and minimizes the out of pocket burden for the owner. It also creates an accountability chain that helps prevent disputes over who paid for what. In practice, you will submit the contractor’s invoices, documentation of work performed, and any change orders that were approved, and the insurer will pay in accordance with the agreed schedule. The process is not always immediate; there can be interim payments for milestones, and there may be holdbacks for unresolved items such as code compliance or weather related delays. The key to smooth cash flow is proactive documentation and timely communication with the insurer, the adjuster, and the contractor.

The repair itself proceeds in orderly steps. First comes the assessment and scoping phase, where the contractor, often after a preliminary walk through, produces a repair plan that details the sequence of work, the needed materials, and the safety measures required to restore the envelope to its pre incident condition. The plan must meet code requirements and, in many cases, address resilience improvements that reduce future risk. Then comes the procurement phase, where the necessary materials and components are sourced. This phase may reveal supply chain constraints or lead times that affect the project timeline. The insurer and the owner discuss contingencies to mitigate downtime, particularly if the building houses tenants who rely on the space for revenue. The next stage is the actual construction, with the contractor performing the approved scope. The work is typically staged to minimize disruption, with temporary shoring or containment to protect the interior of the building and to preserve accessibility for tenants and customers. Throughout this period, the owner monitors safety, quality, and adherence to the agreed budget. The contractor reports progress and flags any changes in scope that would necessitate additional approvals or potential cost adjustments.

When the work is near completion, a final inspection takes place, often by the insurer and sometimes by local authorities to confirm compliance with code and safety standards. Any punch list items must be resolved before final payment. Only then does the building return to service, and the business can resume normal operations. The experience of a truck collision and the subsequent repair process is rarely a linear path. It involves back and forth between investigators, insurers, engineers, and construction professionals. Yet a well managed sequence minimizes downtime and avoids the risk of under repairing the envelope or misallocating resources. The owner who keeps a robust and transparent record, who communicates early and often with the insurer, and who remains engaged with the contractor, is better positioned to navigate disputes, ensure timely completion, and achieve a durable restoration.

An important nuance for owners concerns the potential for subrogation. After the claim is resolved and the trucking party or their insurer pays for the repairs, the at fault party’s insurer may seek to recover some of their costs from the responsible party. This process does not affect your repairs or your coverage, but it is a reminder that the path from incident to settlement can involve multiple layers of legal and financial maneuvering. It reinforces the importance of precise fault determination and documentation, so that money flows smoothly to satisfy the obligations of the responsible party while protecting your own financial position. In that sense, the chain of accountability extends beyond the immediate repair. It shapes the future risk management posture of the building and informs decisions about safety improvements, building envelope strengthening, and tenant communication plans that you implement to preserve business continuity.

If you take away one essential idea from this chapter, it should be this: the person who fixes the building is not automatically the person who caused the damage, nor is the responsibility to pay automatically yours or someone else’s. The resolution hinges on the fault finding and on the policy structures that govern liability and property loss. You, as owner, hold the lever of construction control, the insurer holds the lever of funds, and the at fault party holds the liability exposure. The smooth coordination of these elements requires a disciplined approach to documentation, a clear understanding of policy terms, and a willingness to engage professionals who can translate the legal and financial language into actionable construction work. In parallel with the repair itself, you should keep tenants informed about the timeline and the steps being taken. A transparent communication plan reduces uncertainty, preserves trust, and supports business continuity during a period of significant disruption. The longer the project persists without clarity, the more the perception of risk grows among tenants and customers. A coherent communications strategy complements the technical and financial strategies and helps ensure that the building remains a reliable place for business activities throughout the repair window.

For a broader perspective on how the industry approaches incident claims and repairs, you can explore more insights at the McGrath Trucks Blog. It offers context on common practices, how insurers evaluate claims, and general industry trends that can illuminate the path from impact to restoration. McGrath Trucks Blog.

In the end, the core takeaway is practical and clear. If a truck hits your commercial building, the fix involves a partnership among three pillars: the at fault party or their insurer who should cover the repair costs, your own property insurer who manages the claim and the funding path, and you the building owner who must lead the repair. You determine the scope, select the contractor, and manage the project within the framework of what the insurer deems reasonable and what the policy allows. The final settlement reflects not only the physical act of reconstruction but also the governance of risk and the memory of a disruption that tested your business resilience. The building you own is a structure of systems that must be repaired not only physically but operationally, so that the enterprise can endure and evolve in the wake of the incident. This is not a tale of one party fixing what another broke; it is a narrative of disciplined coordination, transparent documentation, and professional execution that restores safety, functionality, and confidence for every stakeholder involved.

External reference for further reading on how commercial property insurance handles such incidents: https://www.insurance.com/insurance-types/commercial-property-insurance/

Crash, Then Construction: Who Fixes a Commercial Building After a Truck Collision

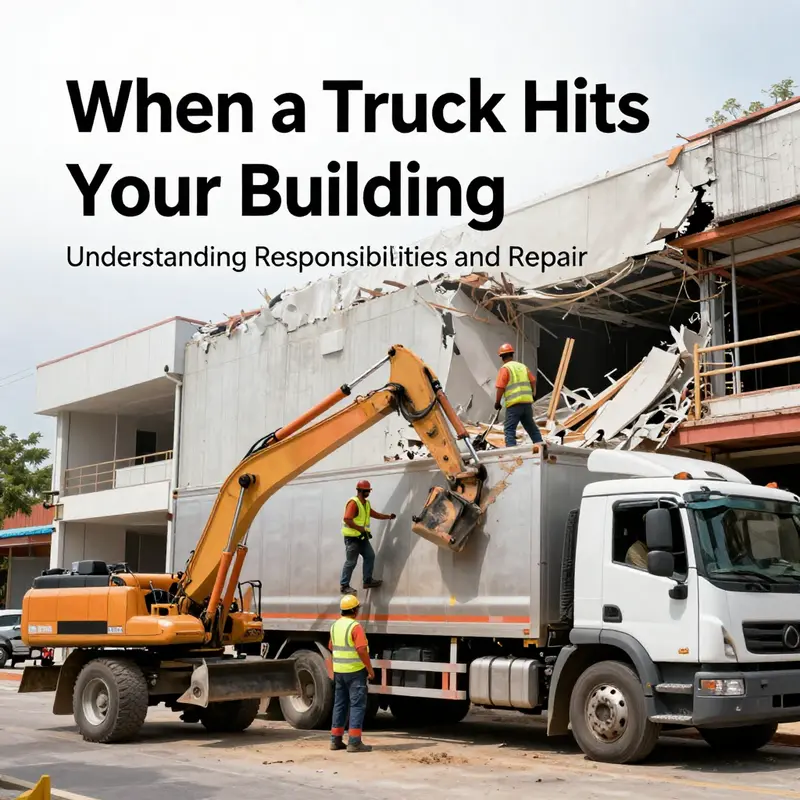

When a truck crashes into a commercial building, the scene is loud with alarms and dust, yet the questions that follow are quieter but heavier: who is responsible for the damage, and who actually does the repair work to bring a business back to life? The answer sits at the intersection of law, insurance, engineering, and the practical tempo of construction. This chapter follows the journey from the moment of impact to the first days of stabilization and the long arc of reconstruction. It is not a tale of luck but of a precise chain of responsibility and a carefully coordinated team that can determine whether a storefront, an office tower, or a warehouse will be restored to its previous function or reimagined for safer operation after the shock of a crash has passed. The central truth is straightforward: in most cases the party at fault bears the duty to pay for repairs, but the road from incident to re-occupation is navigated by a spectrum of players, each with a defined role and a set of responsibilities that must align under the rules of liability, contract, and safety codes.

To understand who fixes a commercial building after a truck collision, one must start with liability. The initiation of this inquiry is grounded in evidence: police reports,现场证据 like photographs and videos, and witness accounts. These pieces help determine whether the truck operator violated traffic laws, whether the driver was distracted or intoxicated, or whether another factor contributed to the crash. When fault is established, the third-party liability component of the truck’s insurance policy typically becomes the primary payer for repairs. In most jurisdictions, that means the at-fault driver’s insurer steps into the claim to cover materials, labor, and related costs up to policy limits. For building owners, this is the starting point that connects the accident to a formal repair pathway. Yet the path is rarely linear. Insurance is not a single-note instrument; it sometimes creates a process that involves the owner’s own commercial property insurer, especially when the damage disrupts business continuity or when the insured amount requires subrogation or recovery from the at-fault party’s insurer.

The practical consequences of liability touch every corner of the repair process. If the truck driver operates as an employee, vicarious liability laws may hold the employer partly or wholly responsible for actions taken within the scope of employment. If the driver is an independent contractor or the operation is managed through a fleet arrangement, the responsibility could be allocated to the vehicle owner or the operator, depending on how contracts and local law allocate risk. In any of these scenarios, the goal remains the same: secure coverage that pays for the damage, including structural repairs and the restoration of interiors where needed. When insurance does not fully cover the costs—perhaps due to policy limits, exclusions, or deductibles—the responsible party may bear the out-of-pocket burden. Those payments can include immediate stabilization measures as well as the more substantial reconstruction costs. The legal landscape is not abstract here; it shapes the choices a building owner makes about who starts repairs, what specifications guide those repairs, and how quickly a building can return to service.

Once liability is determined and coverage is in motion, the real work begins. The role of construction and repair professionals becomes central, because the physical task of returning a damaged building to a safe and usable state is not simply about replacing missing bricks or fresh paint. It is about assessing structural integrity, confirming safety, and ensuring compliance with current building codes. The first practical step is damage assessment, typically led by licensed engineers who can interpret the consequences of the impact beyond visible cracks or displaced facades. Engineers examine whether load-bearing elements—walls, columns, foundations—have been compromised. They may require non-destructive testing, material testing, or, in severe cases, the removal and replacement of damaged sections. Assessments often culminate in an engineering report that becomes the basis for a repair plan. If the work involves structural concerns or alterations that could affect the building’s performance under wind, seismic, or other loads, a detailed plan is essential for both safety and code compliance.

In many places, a set of established technical guidelines shapes how repairs must be designed and implemented. For example, in some jurisdictions, there are recognized guidelines that govern damage repair of load-bearing structures in residential buildings, and those guidelines inform how restorations are evaluated and approved. While the exact regulatory framework varies by location, the principle remains constant: repairs must restore safety margins and ensure that the building can perform as intended under its intended use. This is not merely a matter of reconstructing the facade; it is about reestablishing the structural confidence that tenants, customers, and employees rely on. The engineering phase is followed by the design phase, where architects and structural engineers collaborate to translate the assessment into plans that meet current codes and reflect the realities of the damage. The design must account not only for the immediate fixes but for any necessary upgrades that may be required to bring the building in line with modern safety standards. In this context, the repair plan often becomes a blueprint for what the repair will entail, how long it will take, and how much it will cost.

The actual execution of repairs is carried out by licensed construction and repair professionals, whose work bridges the gap between design and occupancy. Their responsibilities are twofold: restore physical structure and restore business functionality. Physical restoration involves meticulous reconstruction—replacing damaged beams, repairing cracked walls, patching the roof, or reconfiguring access points as needed. It also encompasses the integration of engineering recommendations into real-world anatomy: the installation of temporary supports during stabilization, the careful removal of compromised sections, and the careful reinstatement of structural elements with appropriate materials and workmanship. Operational safety is not secondary; it is a condition of every stage of the project. Contractors ensure that temporary shoring is in place when a building is unstable, that access routes are safe for workers and authorized occupants, and that dust and debris do not create hazards for passersby or neighboring tenants.

The repair process is not one-size-fits-all. The mere fact of a truck impact does not automatically lead to identical remedies across all buildings. Different structures demand different approaches. A building with a straightforward column-and-beam framework may require different attention than a facility with post-tensioned slabs or a complex curtain-wall system. In some cases, a restoration blends with modernization: the opportunity to upgradeFacade elements or to improve energy performance while the shell is open for repair. Each decision affects not only structural safety but also the economic trajectory of the building. For a business, this is more than bricks and mortar; it is about the availability of space for customers, the continuity of operations, and the resilience of the enterprise itself. The repair schedule, therefore, must consider business interruptions, lease terms, and the expectations of tenants who rely on predictable timelines for reoccupation. The owner may seek compensation for lost business income and other indirect losses as part of the overall recovery, recognizing that repair is as much an economic recovery as a physical one.

To ensure that repairs meet safety and performance standards, the process relies on a fluid collaboration among stakeholders. The at-fault party’s insurer, the owner’s insurer, the engineering team, and the construction contractors must coordinate. The engineer’s assessment informs the contractor’s work plan, which in turn must align with the permits and approvals required by local authorities. Permitting processes, inspections, and final occupancy or use approvals mark the transition from construction to usable space. In this sense, the role of repair services extends beyond the wall replacements and roof patches. They are the executors of safety, builders of resilience, and the custodians of the building’s future use. Their work, when paired with the right contract structures and insurance coverage, ensures that the repaired building not only looks like its old self but also operates with the same—or better—safety margins and performance characteristics as before the crash.

The economic and legal dimensions of repair unfold alongside this technical work. A building owner has a legitimate interest in securing full compensation for direct structural damages, but the professional repair process also addresses indirect costs. Lost revenue, rent from displaced tenants, relocation expenses, and the opportunity costs of delayed reopening can all factor into a comprehensive claim. Insurance policy language about business interruption coverage, subrogation, deductibles, and covered perils will shape the possible recovery. The interplay of these elements underscores why timely notification and documentation are crucial. Immediate reporting to the commercial property insurer, prompt coordination with the at-fault party’s insurer, and the compilation of a robust set of evidence—photos, engineering estimates, contractor bids—can improve the chances that the final settlement covers a complete restoration and minimizes prolonged business disruption.

In practice, the sequence from incident to rebuild follows a pattern, though the exact cadence depends on the severity of the damage and the local regulatory environment. Initial stabilization and securing the site take place within days of the crash. This is followed by a formal damage assessment and the development of a repair plan. Permitting and approvals may introduce a temporary pause while the design is refined and inspections are scheduled. Once everything is in place, the construction phase begins, with a sequence of tasks that might include shoring, demolition of damaged elements, structural repair, enclosure restoration, interior repairs, and finally a return to service. If the building houses tenants or has ongoing operations, the owner and contractor work to minimize downtime, sometimes by staging work so portions of the building can remain usable while other sections are rebuilt. Throughout this journey, the building’s safety remains the north star, guiding decisions about materials, methods, and the pace of work.

A nuanced part of this journey is understanding that different legal and professional circles may interpret responsibility and remedy differently. In some cases, the owner’s own commercial property insurance may respond immediately to protect the value of the building and to manage the claim with the at-fault party’s insurer. In other cases, direct negotiations with the responsible party may be pursued, with subrogation possibly pursued later by the owner’s insurer. The guiding principle, however, remains the same: repairs should be funded by the party whose fault caused the damage, and the repair work should restore the building to a condition that is safe for occupancy and compliant with current standards. This is where the practical experience of repair professionals matters most. They translate the financial allocation of responsibility into a concrete plan that respects safety, code requirements, and the owner’s operational needs.

To bring this concept closer to the day-to-day concerns of a business owner facing a truck collision, consider how the story unfolds on the ground. A property owner learns that a truck has struck the building and caused visible damage to the façade and possibly to interior columns or the structural envelope. The first days are about securing the site, documenting everything for insurance records, and communicating with tenants and customers about the temporary disruption. The engineers arrive to perform a preliminary assessment and determine whether the building can be stabilized without full repairs or if immediate structural reinforcement is necessary. The complexity of the job grows if the impact affected not only the exterior shell but also interior systems—electrical risers, plumbing, HVAC ducts, or fire suppression lines. Each system adds its own layer of investigation, procurement, and coordination. The repair team, working under the direction of the property owner and with the support of insurers, then develops a plan that aligns with safety codes and the client’s operational needs. The plan includes not only the physical restoration but also the management of communications with tenants, vendors, and the public to limit reputational and revenue losses during the reconstruction window.

Throughout this process, it is useful to reflect on how different jurisdictions approach repair standards. The technical guidelines used by engineers in complex markets provide a framework for evaluating damage, selecting repair methods, and validating structural integrity after reconstruction. While the specific guidelines may differ, the underlying logic is universal: the repair must restore the building’s load-bearing capacity, ensure durability under foreseeable loads, and maintain compliance with local building codes. In some places, there are additional considerations for the interface between a restored structure and surrounding infrastructure, such as adjacent buildings, sidewalks, and public utilities. The repair team must consider these factors when designing and executing the restoration plan. In this way, the repair work becomes a broader urban resilience effort—one that not only returns a single building to use but also preserves the safety and functionality of the surrounding environment.

As a closing thread for this chapter, it is clear that the question “who fixes commercial buildings after a truck crash?” has a pragmatic answer and a complex set of contributing factors. The party at fault, verified through evidence and legal theory, typically shoulders the financial burden for repairs. Insurance plays a pivotal role in funding those repairs, but the actual physical reconstruction is carried out by licensed professionals who bring engineering insight, code compliance, and practical construction know-how to bear on the problem. The repair professionals do more than replace damaged parts; they reconstitute the building’s safety envelope and its capacity to serve its users. They also help translate the financial settlement into a tangible outcome—an occupied and safe space where business can continue or resume. The path from crash to closure of the project is not merely about restoring a building; it is about restoring trust—the trust that a built environment can recover quickly, safely, and efficiently after a disruption. For readers seeking a concise gateway to ongoing industry perspectives on related topics, our blog offers deeper discussion on the evolving landscape of building resilience and project delivery. our blog.

External resource: https://www.shanghai.gov.cn/nr/zhengce/20231207/85465.html

Final thoughts

In summary, when a truck strikes a commercial building, the responsibility for repairs primarily lies with the truck driver and their insurance provider. However, understanding and navigating the claims and repair processes is essential for business owners impacted by such incidents. By actively engaging with insurance providers and managing the repair process, businesses can ensure minimal disruption and expedite recovery. Always stay informed and prepared to handle these situations effectively.